Economic Abuse and building financial resilience through raising awareness

We understand that debt advice isn’t a tick-box exercise – it’s a journey based on clients’ needs and wants, incorporating safe pathways to advice for Domestic and Economic Abuse as appropriate.

But what is Economic Abuse, and how has the prevalence of this type of Domestic Abuse increased after the incorporation into the Domestic Abuse Act in 2021, which recognised Economic Abuse as a form of domestic abuse for the first time?

Economic Abuse involves behaviours that interfere with an individual’s ability to acquire, use and maintain economic resources such as money, transportation and utilities. It can be controlling or coercive. It can make the individual economically dependent on the abuser, limiting their ability to escape and access safety. It’s designed to intimidate and isolate the victim.[1]

Statistics and data on Economic Abuse disclosures and identification vary significantly across organisations. This variation is influenced by a range of factors, including levels of awareness, quality of training, organisational culture, and the strength of partnership working. Crucially, how economic abuse is defined and understood shapes perceptions of its prevalence. These differing understandings affect the recognition of indicators, the likelihood of disclosure, and, ultimately, how cases are recorded, leading to inconsistencies in the collected data.

Statistics available on Economic Abuse include the following:

- 95% of survivors of domestic abuse have experienced at least one form of economic abuse[2].

- £14.4 billion of UK debt is directly related to economic abuse. On average, a survivor of economic abuse who finds themselves in debt will owe £3,272, with 1 in 4 (24%) having debts in excess of £5,000[3].

- 42% of women who experienced economic abuse didn’t seek help, of which 1 in 5 thought nothing could help[4].

- Nearly 2 in 5 women aged 18-24 experienced economic abuse in the past year[5].

- Nearly 1 million UK women couldn’t leave a dangerous partner due to economic abuse[6].

- 1 in 10 women in the UK state that a partner has put debts in their name and that they had been afraid to say no[7].

- 60% of victim-survivors of coercive control have been coerced into taking out debt, which can take many years to repay and impacts their credit rating[8].

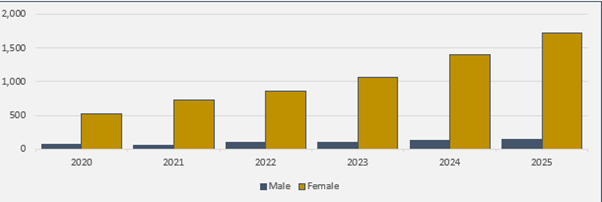

PayPlan’s data correlates with these findings from Refuge and Surviving Economic Abuse, showing the trends in economic and domestic abuse disclosed and identified within debt advice, which evidences a year-on-year increase, culminating in the levels recorded in 2025:

This shows a 32% increase in 2025 alone, and a staggering 210% increase from the levels seen in 2020 – three times higher.

Economic Abuse awareness must be embedded across all organisations to ensure they can support service users safely, practically, and effectively toward the right outcomes. But what if more could be done? By strengthening financial resilience, we could help prevent economic abuse for both current and future victim-survivors. Providing clear, practical steps, alongside accessible guidance on the risks of economic abuse and how to mitigate them, could empower individuals with the knowledge and tools to protect themselves, even before entering a relationship.

Knowledge and awareness are a powerful combination that can be seen as a first step of Economic Abuse prevention, and as a result, could reduce the long-term consequences of this form of abuse and the impact this has on financial awareness in the future. Hence, reducing the resulting ripple effect on mental health, physical health, housing, employment and credit ratings – it’s a non-exhaustive list, and of course, providing overall stability.

The range of the Economic Abuse landscape is vast. It is influenced by abusive behaviours and victim survivors’ experiences – another factor in recognising this form of abuse and acceptance of this behaviour as such, but examples of Economic Abuse in debt advice include, but are not limited to:

- Having sole control of the family income and restricting access to money through limiting access to bank accounts, credit cards and cash

- Preventing claiming welfare benefits

- Interfering with education, training or employment

- Not allowing or controlling access to a mobile phone/transport/utilities/food

- Monitoring spending

- Damage to a property and expecting their partner to pay

- Running up debts in someone else’s name without their knowledge or consent, resulting in damaged credit ratings and affecting future financial resilience.

Given the range of Economic Abuse behaviours experienced by victim survivors, future proofing could be difficult, but adopting good financial awareness practices from an early age, and pre-relationships, as part of good financial habits, could be a game changer in the desire to change many potential victim survivors of economic abuse.

Good practice for us all could be adopting some fundamentals, for example:

- Being aware of your own credit report, credit scores and overall financial awareness and checking regularly to highlight any changes

- Know what is in your name regarding any assets, credit cards, and housing agreements, such as tenancy and mortgage accounts and keep a check on changes on your credit report

- Tech safety starts with knowing your own passwords and PINs, and if you think these have been compromised, change them regularly, or even make this a regular occurrence as best practice -all good habits in the prevention of fraud and scams too

- Being aware that Joint Accounts aren’t mandatory, but if a partner suggests this, ask for both to sign for or agree to transactions in the setup of the account, bearing in mind tech safety. This may not be safe for a victim survivor to do, of course, and safety must always be paramount if this is the case. Awareness of joint account responsibility and 100% liability for both parties on all transactions and overdrafts on the account is also important.

- Keeping important documents in a safe place that you have access to, or know where they are, should you need them

- Applying a notice of correction to your credit report, including password protection, if you are concerned about the risk of Economic Abuse.

Even with adopting these principles, sometimes victim survivors don’t have a choice in these actions, in what is primarily their given right to know about their own finances and accounts and an expectation that these will not be compromised through economic abuse. At this point, it’s important to remember that this won’t always be the case. If someone does feel this kind of control and is worried about having these conversations with their partner, they should reach out for help and support as soon as it is safe to do so.

Keeping ahead of evolving technology that influences economic abuse is a challenge, but adopting some basic principles, as referenced above, to build financial resilience, will be a step in the right direction in raising awareness of economic abuse for victim survivors, and our continued call to action to the financial industry to support these basic principles.

Following on from PayPlan’s and Refuge call to action in 2025, the financial industry needs to play its part in not only supporting victim survivors of economic abuse but identifying this form of abuse when there are clear flags that this is the case, through preventing further economic abuse from taking place, or, to be allowed to happen in the first instance – either through the actions of the perpetrator or through policies and procedures that do not meet the needs of the victim.

Measures from the Financial Industry that could be taken, based on lived experience feedback from victims’ survivors at PayPlan, include:

- Writing off debt that has resulted from economic abuse as a solution that not only removes the debt that has arisen from economic abuse but understands and removes the barriers of having to provide crime reference numbers, police reports, income and expenditures, medical documentation and perpetrator personal details where these are not available due to the economic abuse or would compromise safety, and to drive policy to accept other communications, such as a letter from a Domestic Abuse organisation and or a debt advice provider to evidence the economic abuse.

- Updating credit reports to reflect debt that has been removed and that does not cause any further financial harm through the impact of a negatively affected credit score.

- Support with financial disassociation with joint accounts and credit reports, and sharing information on how this can be done safely through a credit reference agency

- Where joint accounts have been taken out without the victims’ survivors’ knowledge, the liability of the debt has been removed from the individual impacted by the economic abuse.

- Accounts devised specifically for victim survivors to remove the barriers of access and proof of identification, whilst ensuring additional security layers and specific communication routes to highly trained advisers.

- Highly trained Specialist Advice Teams that follow a tell us once approach and provide consistency through working with an adviser on a one-on-one approach, offering appointments at a time and length that accommodates needs and a choice of adviser gender to remove barriers to make the survivor more comfortable, which without could be triggering, and a barrier to accessing support.

- Access to language interpreting services for clients who do not speak/read English, as standard, not relying on a friend, family member, partner or spouse to be an interpreter.

- Enhanced security checks when accounts are opened, such as facial recognition to reduce the risk of economic abuse, fraud and scams.

- Consequences to the perpetrator with credit report markers, when economic abuse has been identified as a preventative measure due to the financial impact this could have on future financial decisions and resilience.

This list has the potential to develop as we see further integration of AI into debt advice and financial services, and a consequent increased risk of economic abuse, given the link between the two and the levels already seen at Refuge:

Fact: 1 in 3 UK women (36%) have experienced online abuse or harassment, rising to almost 2 in 3 among young women aged 18–34 (62%). We know that 1 in 6 (16%) of these women experienced this abuse from a partner or former partner.[9].

Fact: Some groups of women are disproportionately affected by tech-facilitated abuse. Our Unsocial Spaces (2021) report found that 75% of LGBTQIA+ women had experienced online abuse, alongside 45% of women from ethnic minority backgrounds.[10].

Fact: Tech-facilitated abuse is on the rise, and between 2018 and 2024, Refuge’s dedicated Technology-Facilitated Abuse and Economic Empowerment (TFAEE) team experienced a 205% increase in referrals[11].

With the incorporation of AI and the potential impact on Victim Survivors, an additional concern is the lack of human response to a disclosure around domestic and economic abuse and the language used in its response – or the indicator of economic abuse not being identified – all of which could be a barrier and blocker to a victim survivor accessing support in the future The FCA announced in January 2026 that they will be conducting a review into how advances in AI and technology will impact financial services markets, firms and consumers to 2030 and beyond and will consider the current landscape and evidence – the current prevalence of Economic Abuse needs to be at the heart of this review.

PayPlan and Refuge have been working in partnership to educate the sector on Economic Abuse, but also to help protect and support Victim Survivors. In 2021, together they launched their Safe Pathway into Debt Advice, and now, in a world of emerging AI use, a further review is needed to identify these additional risks and how they can be mitigated throughout a client journey. Both organisations have committed to working on this review during 2026.

If anything you have read above has concerned you, or you would like further support, the organisations below are here to help.

- REFUGE – Refuge, the UK’s largest specialist domestic abuse organisation

- Women’s Aid

- Surviving Economic Abuse

- PayPlan

[1] Economic Abuse Toolkit (HTML) – GOV.UK

[2] Facts and Statistics – Refuge

[3] Facts and Statistics – Refuge

[4] Changing-Systems-Saving-Lives-2025-2028-Strategy-Surviving-Economic-Abuse.pdf

[5] Changing-Systems-Saving-Lives-2025-2028-Strategy-Surviving-Economic-Abuse.pdf

[6] Changing-Systems-Saving-Lives-2025-2028-Strategy-Surviving-Economic-Abuse.pdf

[7] SEA-Coerced-Debt-Statistics-08-2020-Final-1.pdf

[8] SEA-Coerced-Debt-Statistics-08-2020-Final-1.pdf

[9] Facts and Statistics – Refuge