The Regulation of Buy Now Pay Later and the risk of unintended consequences:

Table of contents

At PayPlan we welcome the regulation of Deferred Payment Credit (DPC), better known as Buy Now Pay Later (BNPL), by the Financial Conduct Authority (FCA). However, this development also raises concerns about the impact on consumers who rely on this form of credit. Many people use BNPL to manage cost-of-living pressures, navigate the current economic environment, and maintain their standard of living. In many cases, this includes funding everyday expenses such as food, including takeaways, clothing and discretionary purchases such as holidays and other luxuries, as well as unexpected costs such as the replacement of broken household appliances.

What is BNPL and what will the new regulation bring?

BNPL is a type of short-term credit that allows you to delay payment – usually by splitting a purchase into smaller instalments over a set period. It’s widely offered at online checkouts and often promoted as interest-free.

It is quick, convenient and hasn’t always involved a formal credit check.– but that’s all about to change.

The change in regulation, on the 15th of July, will mean that BNPL providers will need to provide certain information and support their customers in a way that may not have been the standardised approach before.

The FCA has referenced that many consumers don’t realise that BNPL is classed as credit and aren’t aware of certain consequences such as late payment fees of taking out these agreements. An example of one such consequence is the late payment fees associated to these accounts, so the FCA requirements to the new regulation will include information that needs to be issued before a BNPL agreement is taken out, with the aim being to support consumers with their decision making as to whether this form of short term credit is affordable, but also sustainable , and therefore better financial outcomes in the longer term:

This information will consist of:

- The amount that’s borrowed.

- When repayments will need to be made.

- How much the repayments will be.

- How much any late fee/s will be

- The rights and protections in place for a consumer

Further measures by the FCA will include:

- Affordability checks demonstrating sustainability, and proportionate assessments which shouldn’t add friction for the consumer

- Ensure that lending is managed and consumers avoid taking on excessive and unaffordable debt

- Referring to debt advice where financial difficulty is identified

In a recent Money Advice Liaison group meeting a representative from the FCA provided some further context as to why BNPL should be regulated. This included that in their recent findings they found that BNPL is the third most popular use of consumer credit and that the Consumer Duty and outcome-driven concept has played a big part in how firms will be regulated.

Following the introduction of regulation, and new affordability checks the FCA expect BNPL transactions to decrease but that the industry will continue to grow in a sustainable way due to the range of products and items that BNPL can be used for. The question is, will this transactional decrease be at risk of causing harm to consumers currently using this type of credit for basic needs and failing affordability checks, and then other forms of credit not being an affordable option?

Vox Pops and Consumer Insights into BNPL

We recently conducted Vox Pops, otherwise known as ‘the voice of the people’, giving some fascinating insights into its BNPL usage and consumer experience.

Insights included:

- 85% of consumers interviewed had not heard about the new FCA regulations for BNPL.

- 15% only knew a little about the new regulations – these consumers had learnt about the new regulation by listening to a news bulletin. 100% of consumers interviewed thought regulation was needed, and it was a good idea for this form of credit.

- 62% of consumers interviewed had used BNPL for larger purchases. Washing machines, laptop, dishwashers and televisions were some of the items mentioned that had been purchased.

- 38% of consumers interviewed had not used BNPL.

Comments as further insight included:

“I have used BNPL, but it has got me into a lot of problems as it’s easy to forget about what you owe and lose track of payments.”

“It was a softer check, so it was easy for me to get the credit, even though I had a poor credit rating due to CCJ’s.”

“It’s a good idea –but not if you don’t have the money to make the payments.”

Another consumer referenced that they do use BNPL but tries to limit usage, as it’s a difficult cycle to get out of once you are in it and one consumer said that they have used it as a way of getting the things you want straight away, so its instant gratification.

A different perspective was given from one consumer as they used BNPL for budgeting, as they know they will be returning items from an online retail order, so it supports with their cash flow and spending and one consumer said “Buy Now Pay Later is a sign that if I can’t afford it , I shouldn’t be buying it”, and there were other comments made that because using BNPL had got them into financial difficulty in the past it has changed the way they buy things, so they now save for things, and buy them outright.

The consumer insights gained from these Vox Pops were certainly mixed, but conclusions can be drawn under the following summary areas as follows:

- Awareness & Regulation

- Very low awareness: 85% of consumers had not heard of upcoming FCA regulation on BNPL.

- Only 15% had limited awareness, primarily via news bulletins.

- Universal agreement: 100% of participants supported regulation, viewing it as necessary and positive.

Implication:

There is a significant consumer knowledge gap, despite strong appetite for safeguards. This new regulation will aim to meet that appetite as consumers will be provided with clearer communication and information to support them in making effective and informed decisions, and reach the best outcome

- Usage Patterns

- 62% have used BNPL, mainly for essential or high-cost goods, including washing machines, laptops, dishwashers and televisions.

- 38% have never used BNPL.

Implication:

BNPL is used not only just for discretionary spending but increasingly for household essentials, indicating financial pressure and reliance on credit for basic needs.

- Consumer Experience & Risks

Recurring themes highlight behavioural and structural risks:

- Lack of visibility and control.

- “Easy to forget what you owe and lose track of payments.”

- Accessibility for vulnerable consumers

- “Softer checks” enabling access despite poor credit history (e.g. CCJs).

- Debt spiral concerns

- Described as “the Devil” and “taking advantage of poor people.”

Implication:

BNPL design features (ease, low friction, limited checks) may contribute to over-indebtedness and vulnerability, reinforcing regulatory concerns.

- Mixed Consumer Perception

Consumers showed balanced but cautious views:

Positive / functional uses:

- Helps with budgeting and cash flow

- Useful for managing returns in online shopping

- Provides flexibility for spreading costs

Negative / behavioural risks:

- Drives instant gratification

- Creates a cycle that is difficult to exit

- Acts as a signal of affordability issues

Behavioural change noted:

- Some consumers reported learning from past harm, now:

- Avoiding BNPL

- Saving and purchasing outright

Implication:

BNPL is seen as both a tool and a risk, with outcomes heavily dependent on consumer behaviour and financial resilience.

Overall Strategic Insight

- High support for regulation + low awareness = urgent need for consumer education and engagement

- BNPL is increasingly embedded in everyday financial coping strategies, particularly for vulnerable customers

- There is clear evidence of harm pathways, especially linked to:

- Ease of access

- Lack of transparency

- Behavioural triggers (instant gratification)

- These conclusions from conducting these Vox Pops are further endorsed by the scale of consumer usage seen in our customer data.

Rising BNPL and what our customer data shows

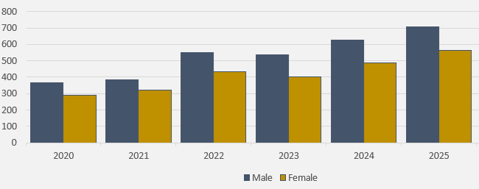

We have seen the results of BNPL usage increase over the last 5 years as the following graph shows:

- This data shows that BNPL usage for our customers has increased by a staggering 3793% from 2020 to 2025.

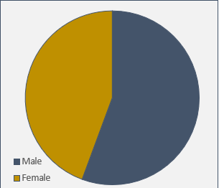

- Men have more BNPL accounts than women with a 51% and 41% split respectively – 8% of this data is unknown as clients have preferred not to share this information.

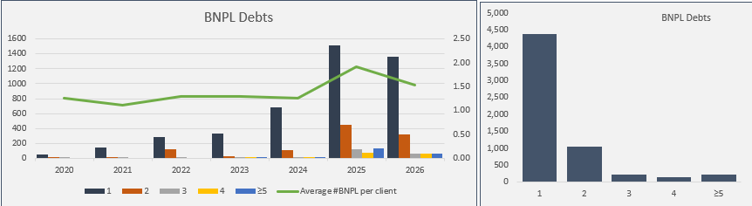

- In 2020, for customers using BNPL, the average number of accounts for this form of credit was 1.25 increasing to 1.91 accounts in 2025.

- In 2025 66% of consumers had 1 account, 20% had 2 accounts, 5% had 3 accounts, 3% had 4 accounts and 6% had 5 accounts or more.

This is summarised as follows:

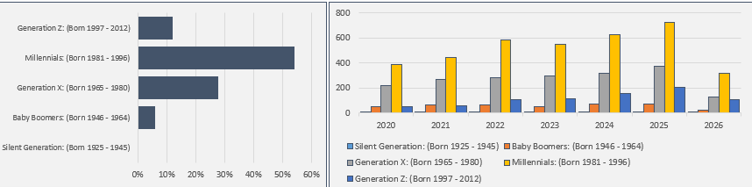

Our data also tells us, that whilst all age demographics have disclosed using this form of credit, it is the millennials that are most likely to use this, resulting in 54% of all disclosed usage, followed by Generation X at 28%, and Generation Z at 12%. The baby boomers and silent generation make up the remaining 6% with the silent generation under 1% of that total.

UK finance shared their own findings in a report released in November 2025: BNLP trends in the UK: growth, usage and regulatory challenges (1)

This report stated that usage of BNPL had increased in 2024 as 25% of UK adults used BNPL at least once during that year, compared to 14% in 2023. This mirrors the rise of customers seen at PayPlan with this form of credit.

This report also shows that the demographic groups using BNPL have broadened over time, from primarily female usage when BNPL was first launched, to being used by both genders.

Additionally, this report found young consumers to use BNPL more than older demographics, highlighted in the PayPlan data.

Alternative credit solutions

In addition to BNPL accounts, we also know that our customers are accessing other forms of short-term credit, including support available at a local level, and with over a third of clients using short term credit, owing money to a credit union.

Customers also on occasion, bravely share with their debt advisor that they have borrowed from a loan shark, and although these are low recorded volumes due to the barriers to disclosure, year on year, we’ve seen an increase, resulting in 2025 being the highest year on record for loan shark usage identified and disclosed.

![]()

We anticipate that the usage volumes of these alternative credit solutions will increase due to the regulation of BNPL and the impact this may have on individuals who fail affordability checks yet need essential items and are able to provide for and support their families.

As part of PayPlan’s wider support initiatives, and reacting to the rise in loan shark disclosures, we became a recognised partner of the Stop Loan Sharks campaign with the Illegal Money Lending Team and became the first debt advice organisation in 2025 to achieve Partner Plus status.

Included in this partnership accreditation was ensuring that PayPlan advisers were trained to identify and react to any indicators of loan shark activity, including the FRIENDS framework to assist with asking questions and building trust with their client, to reach a point of disclosure. This has been supported by the increase of customers being identified as using this form of illegal lending and gaining support from the Illegal Money Lending Team through the referral route we have in place, to provide help and guidance for this wider support need.

Strategic focus areas to support customers impacted by the new regulation

Given the trepidation around the regulation of BNPL and the potential impact on people using this credit facility, key strategic focus areas have been identified to support customers moving forward.

These strategic focus areas will include:

- Consumer Education

- Raising awareness of FCA regulation and rights

- Vulnerability Identification

- Strengthening identification where BNPL is masking financial distress

- Policy & Advocacy

- Use insights to support stronger affordability checks and safeguards to prevent consumers taking on excessive and unaffordable debt

- Internal Insight Integration

- Align BNPL behaviours with our vulnerability and support frameworks.

The FCA state; “We want our regulatory regime for DPC to reduce the risks of harm to consumers. We want to be proportionate so that the DPC market can continue to innovate and grow sustainably, and that consumers can still access DPC where appropriate. (2).

With this aim of reducing risks of harm to consumers, this also brings an additional responsibility for financial organisations, including the debt advice sector, to respond to the aim of reducing the risk, through a robust strategy, to enable their customers to be not only aware and educated of the change, but also how to manage the change, and the impact this may have.

In a cost-of-living crisis, which appears to be the new economic landscape, these strategies need to be robust and sustainable, with the needs and wants of consumers in mind at all times.